核心要点

澳大利亚4月牛肉出口量达140943吨,同比2025年4月增长11%;

北美依旧为最大出口市场,出口量同比上涨12%;

中国大陆市场增长势头强劲,草饲牛肉与特选谷饲牛肉出口量均大幅攀升。

澳大利亚4月牛肉出口量较3月有所回落,但仍显著高于去年同期水平。当月总出口量140943吨,较3月下降6%,较2025年4月同比增长11%。

2026年前四个月,澳大利亚牛肉累计出口量506138吨,较2025年同期增加16%。

4月冷藏、冷冻牛肉出口量均同比上涨11%;其中草饲牛肉出口增12%,谷饲牛肉出口增8%。

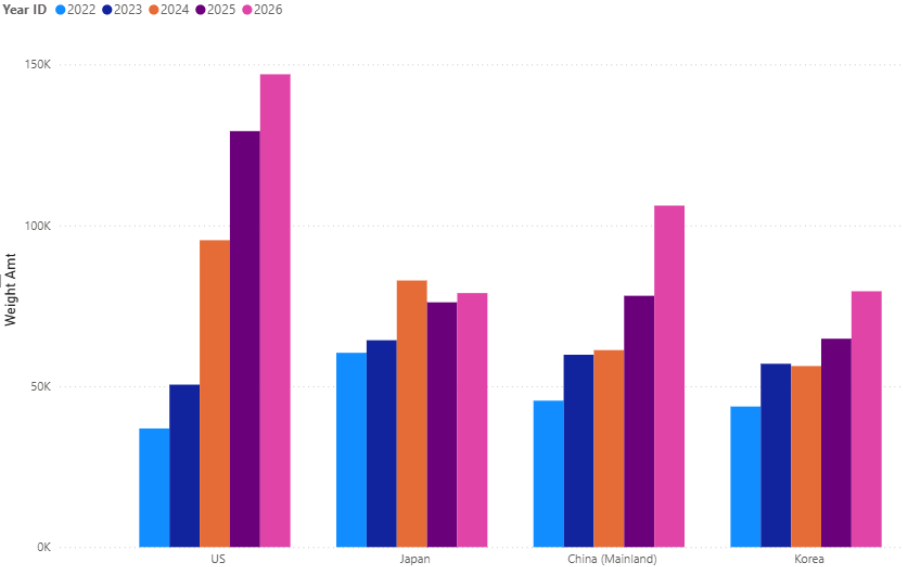

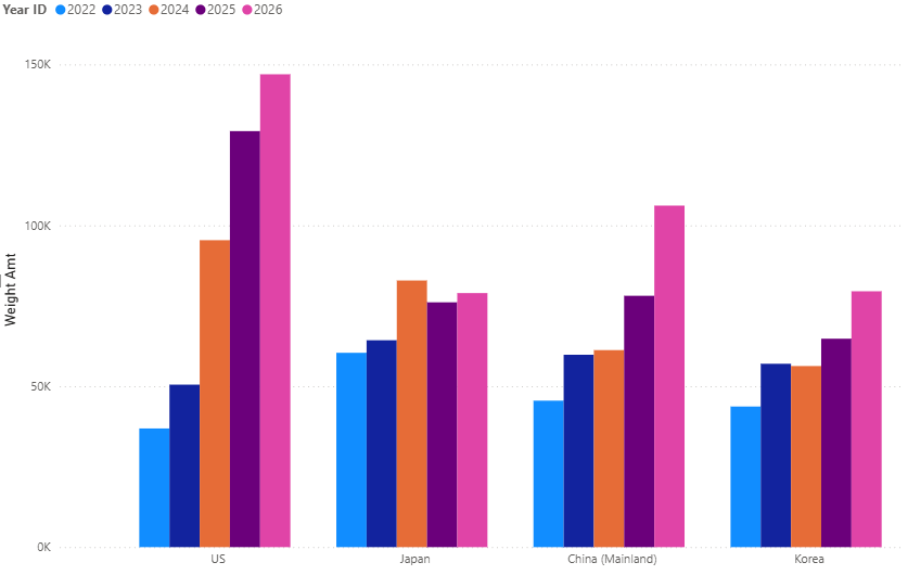

1–4 月牛肉前四大出口市场(来源: DAFF)

北美市场

4月北美仍是澳大利亚牛肉第一大出口市场,到货量45992吨,较3月下滑 2%,较去年4月同比增长12%。

美国占据绝大部分份额,当月进口澳牛41173吨,同比上年4月上涨11%。今年截至目前,澳对美牛肉累计出口装运重量达146951吨,已超越2015年全年144270吨的纪录。

4月澳对北美冷藏牛肉出口13645吨,同比增长25%;冷冻牛肉出口32347吨,同比增长8%。贸易结构仍以草饲牛肉为主,出口量44220吨,同比上涨14%;谷饲牛肉出口量1771吨,同比下滑21%。

2026年前四个月,澳对北美牛肉累计出口 163132吨,较2025年同期增长16%。

中国地区

在主要出口市场中,中国地区同比增幅最高,为年内开局表现最强市场。4月澳对中国牛肉出口32347吨,较3月下降 8%,较 2025年4月大幅增长 32%。

出口商赶在保障措施配额用尽前提前出货,支撑了2026年开局高景气行情,推升对华年初发运量。前四个月澳对大中华区牛肉累计出口116201吨,较 2025年同期增长30%。

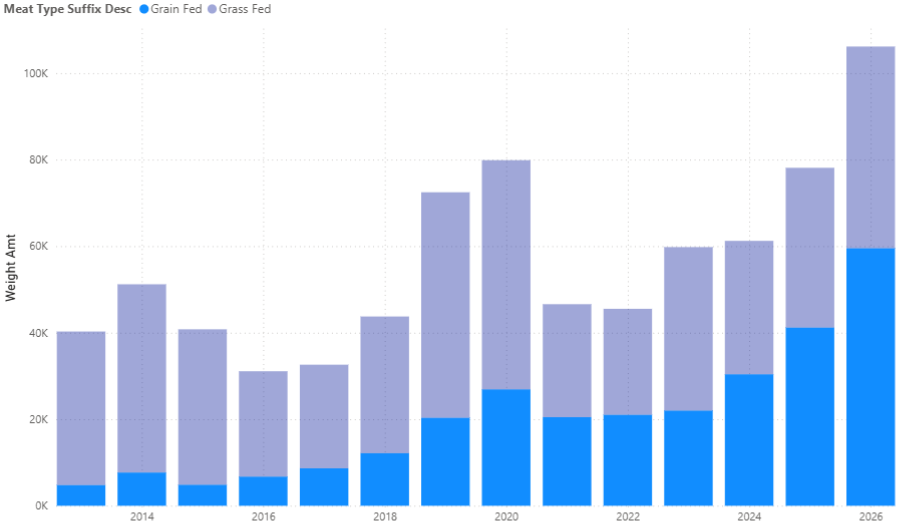

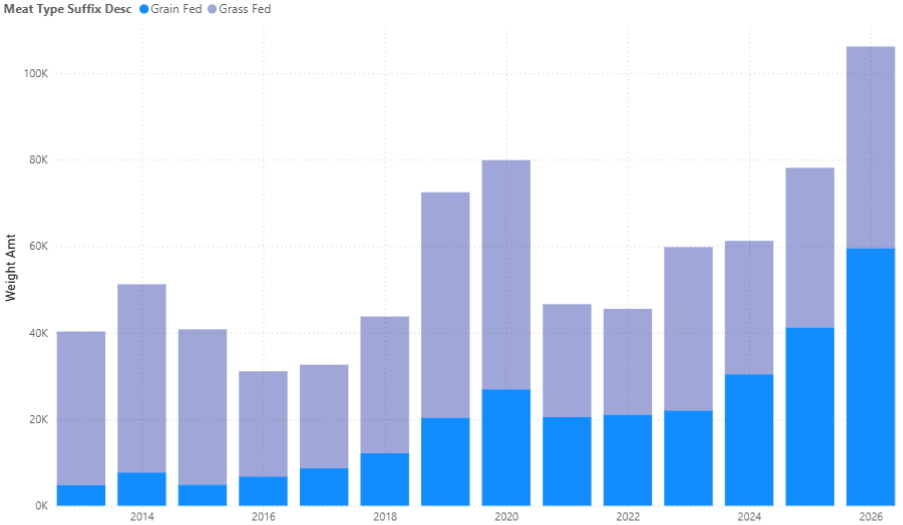

1-4 月 对华牛肉分品类出口统计(来源: DAFF)

4月中国大陆进口量为区域主力,达29572吨,同比上年4月增长38%,是拉动区域增长的核心动力。反观中国台湾地区,当月进口澳牛2136吨,同比下滑 15%。

各类牛肉全面普涨,草饲、谷饲对华出口均大幅走高:草饲牛肉累计对华出口46616吨,同比增长 26%;谷饲牛肉增幅更为突出,累计出口59530吨,同比大涨45%。

2026年前四个月,谷饲牛肉占澳对华牛肉出口总量略超半数,体现谷饲需求旺盛;近三年整体出口量累计增幅达 171%。草饲牛肉依旧保持可观体量,两种养殖品类共同拉动对华出口同比增长。

日本与韩国市场

4月澳对日本牛肉出口表现偏弱,总量20504吨,较3月下降 14%,较去年4月同比下滑4%。草饲、谷饲牛肉对日出口均同比回落,分别下降4%、5%。尽管4月走弱,前四个月澳对日牛肉累计出口78956吨,仍较2025年同期高出4%。

4月澳对韩国牛肉出口22365吨,较3月回落12%,较2025年4月同比增长11%。增量主要由冷冻牛肉和草饲牛肉拉动,冷冻品类出口增14%,草饲品类增24%。前四个月澳对韩牛肉累计出口79518吨,同比大增23%。

整体来看,4月澳大利亚牛肉出口虽环比3月回落,但依旧高于去年同期,全年有望创下出口纪录。北美持续占据最大出口份额,大中华区则实现强势开局。

撰稿人:埃米利亚诺・迪亚兹 澳大利亚肉类及畜牧业协会(MLA)高级市场信息分析师本报告信息截至 2026 年 5 月 7 日撰写时点有效。

免责声明:澳大利亚肉类及畜牧业协会不对本报告所载信息的准确性、完整性及时效性作出任何保证。使用者依据本报告内容所作决策,风险自行承担,协会不对由此产生的任何损失及损害承担相关责任。

消息来源:MLA

April beef exports above year-ago levels

Key points

Australian beef exports reached 140,943 tonnes in April, 11% above April 2025.

North America remained the largest market, with exports up 12% YoY.

Mainland China recorded strong growth, with both grassfed and specially grainfed exports lifting sharply.

Australian beef exports eased from March to April but remained well above year-ago levels. Total exports reached 140,943 tonnes, 6% lower than March but 11% higher than April 2025.

For the first four months of 2026, Australia exported 506,138 tonnes of beef, 16% more than the same period in 2025. Chilled and frozen exports both lifted 11% year-on-year (YoY) in April, while grassfed exports rose 12% and grainfed exports increased 8%.

Top four beef export markets (January to April) Source: DAFF

North America

North America was Australia’s largest beef export market in April, receiving 45,992 tonnes. This was 2% lower than March but 12% higher than April 2025.

The United States accounted for most of the volume, with exports reaching 41,173 tonnes, 11% above April last year. For the year-to-date (YTD), exports to the US surpassed 2015 (144,270 tonnes shipped weight (swt)) with a total export of 146,951 tonnes swt.

Chilled exports to North America increased 25% YoY to 13,645 tonnes, while frozen exports rose 8% to 32,347 tonnes. Grassfed beef continued to dominate the trade, lifting 14% YoY to 44,220 tonnes. Grainfed exports fell 21% to 1,771 tonnes.

For the YTD, exports to North America totalled 163,132 tonnes, 16% above the first four months of 2025.

Greater China

Mainland China recorded the strongest YoY growth among the major markets listed, and the strongest starting year. Australia exported 32,347 tonnes of beef to the region in April, 8% lower than March but 32% higher than April 2025.

The strong start to 2026 has been supported by exporters moving product into China before the safeguard quota is filled. This has contributed to higher early-year shipments and lifted YTD exports to Greater China to 116,201 tonnes, 30% above the first four months of 2025.

Mainland China accounted for the majority of the April volume, receiving 29,572 tonnes. This was 38% higher than April 2025 and was the main driver of growth across the region. By contrast, exports to Taiwan fell 15% YoY to 2,136 tonnes.

Beef exports to Mainland China by fed (January to April) Source: DAFF

Growth was broad across product categories, with both grassfed and grainfed beef recording strong increases. Grassfed exports to Mainland China rose 26% YoY to 46,616 tonnes, while grainfed exports experienced the largest increase, lifting 45% to 59,530 tonnes.

Grainfed beef accounted for slightly more than half of total exports to Mainland China in in the first four months of 2026, reflecting the strength of demand across that category and underpinning the overall beef export volume growth over the last three years with at 171%. Grassfed volumes also remained significant, with both production systems contributing to the region’s YoY growth.

Japan and South Korea

Exports to Japan were softer in April, totalling 20,504 tonnes. This was 14% lower than March and 4% below April 2025. Both grassfed and grainfed exports eased YoY, down 4% and 5% respectively. Despite the April decline, YTD exports to Japan remained 4% above the first four months of 2025 at 78,956 tonnes.

South Korea received 22,365 tonnes of Australian beef in April, 12% lower than March but 11% higher than April 2025. The YoY increase was led by frozen and grassfed beef, with frozen exports up 14% and grassfed exports up 24%. YTD exports to South Korea reached 79,518 tonnes, 23% above the same period in 2025.

Overall, April beef exports were lower than March but remained ahead of year-ago levels and on track for a record year. North America continued to account for the largest share of exports, while Greater China’s strong start to the year.

Attribute content to: Emiliano Diaz – MLA Senior Market Information Analyst. Information is correct at time of writing on 7 May 2026.

MLA makes no representations as to the accuracy, completeness or currency of any information contained in this publication. Your use of, or reliance on, any content is entirely at your own risk and MLA accepts no liability for any losses or damages incurred by you as a result of that use or reliance.

Source:MLA