核心要点

澳大利亚3月季度牛肉产量达730077吨,创下一季度产量历史新高

肉牛屠宰量230万头,同比增长6%

维多利亚州单季牛肉产量位居全国首位

澳大利亚统计局最新数据显示,2026年一季度牛肉产业开局表现创下历史最佳,产量、屠宰量及交易金额均同步上涨。

今年三月季度牛肉产量达730077吨,较去年十二月季度环比增长2%,同比增幅8%,刷新一季度产量纪录,体现肉牛出栏供应规模持续扩大。

继2025年产量创下高位后,行业产销流转势头在新年延续。全球市场需求旺盛,加之澳洲北部气候条件适宜,推动屠宰加工量稳步走高。

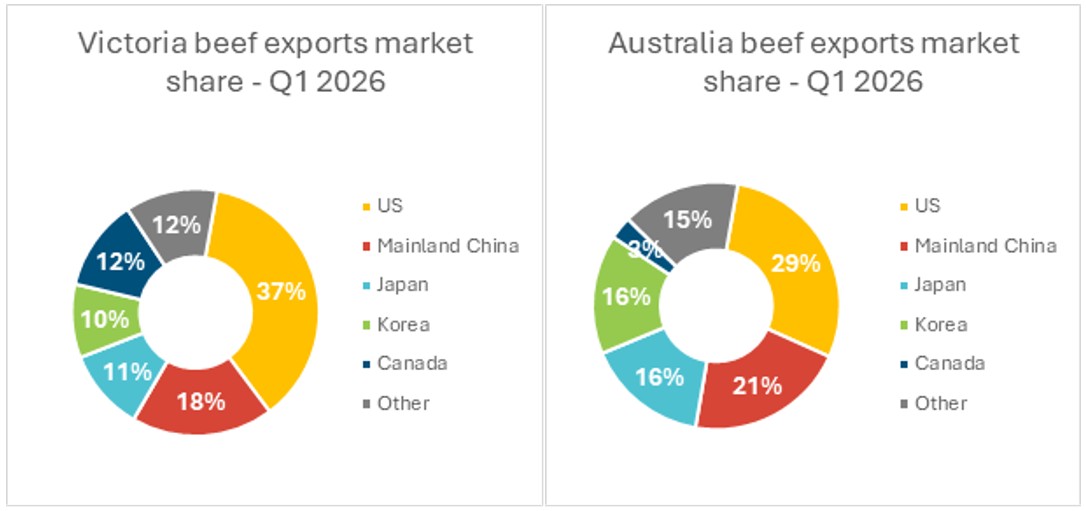

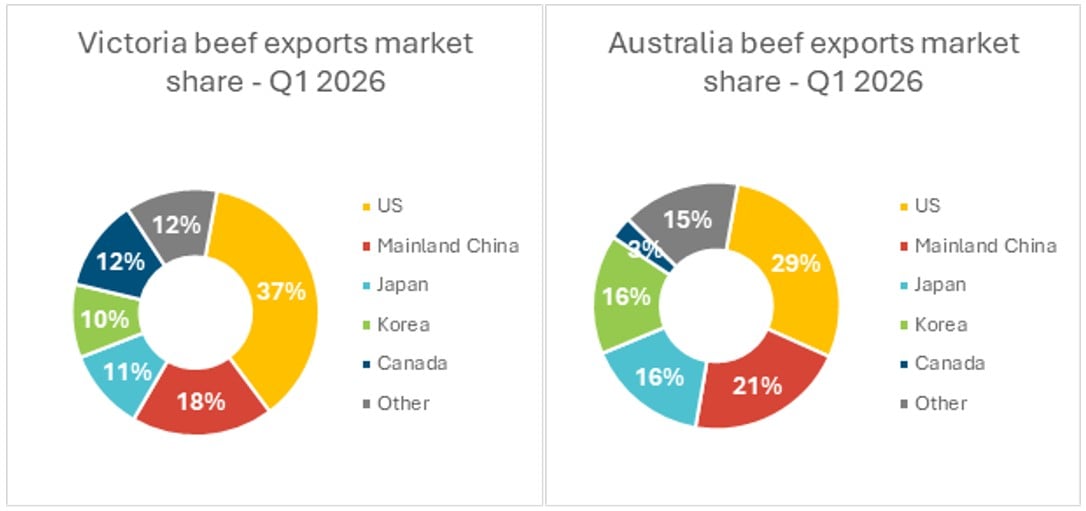

昆士兰州产量占全国总量43%,位居各州之首。维多利亚州增长势头强劲,环比上升4%,较2025年一季度增长10%,折合胴体重量167401吨,创下该州单季产量历史峰值,其产量已连续五个季度稳居全国前列。该州牛肉主要出口北美地区,当地消费需求旺盛,本季度对华出口规模也同步增长。

数据来源:澳大利亚农业林业渔业部

屠宰规模助推产量增长

一季度肉牛屠宰量达230万头,同比2025年同期增长6%,核心产区肉牛供给储备充足,供货渠道保持通畅。

新南威尔士州北部气候偏干旱,促使该地区季末肉牛集中上市出栏量走高。

屠宰量环比微增0.2%,而牛肉产量环比提升2%,得益于肉牛胴体重量持续上涨,本季度均值达317公斤。适宜的气候条件叠加季度谷饲牛出栏量突破百万头历史峰值,共同推动产量走高。

各州屠宰趋势好坏参半

本季度各州屠宰走势分化,体现各地气候与供货条件存在差异

昆士兰州屠宰量增长1%至95.1万头,依旧为屠宰加工第一大州

维多利亚州上涨2%,达55.29万头

新南威尔士州小幅回落1%,降至53.9万头

西澳降幅最大,下跌8%至11.22万头

南澳下降1%,为8.58万头

塔斯马尼亚逆势上扬5%,屠宰量6.1万头

数据显示全国肉牛屠宰总量维持高位,但各州出栏供给分布不均。地域环境持续影响出栏节奏,也左右加工厂货源供给。

一季度业绩延续2025年行业向好态势,2026年肉牛产业开局根基稳固,产量走势契合行业年度预期。不过下半年变数增多,气象预判偏差,叠加对华保障配额相关贸易格局变动,行业不确定性有所上升。

内容供稿:澳大利亚肉类及畜牧业协会高级市场信息分析师 埃米利亚诺·迪亚兹

信息编撰于2026年5月21日

澳大利亚肉类及畜牧业协会(MLA)不对本刊物所载任何信息的准确性、完整性及时效性作出任何保证。用户使用或依赖本刊物任何内容,风险自行承担;因使用或依赖相关信息所造成的任何损失与损害,MLA概不承担任何责任。未经MLA事先书面许可,本刊物任何内容不得擅自转载、复制。凡使用MLA刊物、报告及相关信息,均须遵守MLA市场报告及信息使用条款。

消息来源:MLA

Beef sector surges into 2026 with a new production record

Key points

Australia produced 730,077 tonnes of beef in the March quarter, the largest first quarter beef production result on record.

Cattle slaughter reached 2.30 million head, up 6% year-on-year.

Victoria registered the highest beef production in a quarter.

According to new Australian Bureau of Statistics data, the first quarter of 2026 has been the strongest start to the year on record for the beef sector, with production, slaughter and transaction values all lifting.

Australia produced 730,077 tonnes of beef in the March quarter, up 2% on the December 2025 quarter and 8% higher year-on-year. This marks the largest first-quarter beef production result on record and reinforces the scale of cattle supply moving through the system.

The result follows record production levels in 2025 and shows the sector has carried strong throughput into the new year. High processing volumes were driven by an intense global demand, sustained by a continuation of favourable seasonal conditions across northern Australia.

Queensland led the volumes, accounting for 43% of the total production. Victoria led the growth, with a 4% increase quarter-on-quarter (QoQ) and a 10% lift on Q1 2025, achieving the highest production quarter ever recorded at 167,401 tonnes cwt. This volume was achieved after five consecutive quarters in the top five volumes. With Victorian exports skewed towards North America, this shows the strength on the demand from this market, while Mainland China has also grown this quarter.

Source: DAFF

Slaughter supports production growth

Cattle slaughter reached 2.30 million head for the March quarter, a 6% increase on the March 2025 quarter. The lift confirms a strong supply pipeline, with cattle availability remaining high across key producing regions.

The dry conditions in northern NSW have also contributed, at the end of the quarter, to higher yardings and turn-off in that region.

While slaughter numbers increased 0.2% QoQ, the 2% lift in beef production was underpinned by the lift in carcase weights that continued to trend higher, reaching 317kg in the March quarter. Sustained favourable seasonal conditions and a high level of grainfed turn-off (which achieved a record of one million during the March quarter) supported this result.

State slaughter trends mixed

State-by-state slaughter trends were mixed during the quarter, reflecting different seasonal and supply conditions across the country.

Queensland slaughter lifted 1% to 951,000 head, maintaining its position as the largest processing state.

Victoria rose 2% to 552,900 head.

NSW eased slightly, down 1% to 539,000 head.

WA recorded the largest fall, down 8% to 112,200 head.

SA eased 1% to 85,800 head.

Tasmania moved against the broader southern trend, lifting 5% to 61,000 head.

These movements show that while national cattle slaughter remains elevated, supply is not moving evenly across all states. Regional conditions continue to shape turn-off patterns and processor access to stock.

The March quarter results build on the strong momentum seen throughout 2025, placing the beef sector on solid footing at the start of 2026. Production levels are aligning with MLA’s 2026 Cattle Industry Projections. However, uncertainty is building for the second half of the year, with less favourable weather forecasts and changing trade dynamics following Australia’s use of China’s safeguard quota.

Attribute content to: Emiliano Diaz, MLA Senior Market Information Analyst.

Information is correct at time of writing on 21 May 2026.

MLA makes no representations as to the accuracy, completeness or currency of any information contained in this publication. Your use of, or reliance on, any content is entirely at your own risk and MLA accepts no liability for any losses or damages incurred by you as a result of that use or reliance. No part of this publication may be reproduced without the prior written consent of MLA. All use of MLA publications, reports and information is subject to MLA’s Market Report and Information Terms of Use.

Source:MLA