核心要点

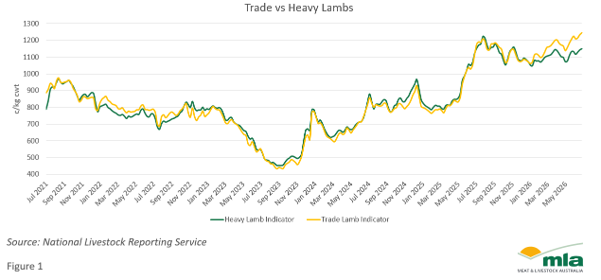

商用羔羊相对重型羔羊每百公斤溢价扩大95美分,创五年多新高。

市场商用羔羊上市量远低于均值,重型羔羊供货量保持稳定。

部分出口市场需求走弱叠加屠宰加工产能不足,制约价格进一步上涨。

季节与供应

南部核心绵羊产区气候适宜、牧草长势旺盛,养殖户得以兼顾羔羊增重,同时抓住羔羊价格创历史高位的行情红利。相较往年,市场出栏羔羊的售卖体重明显提升。

受高额收益驱动,养殖户普遍育肥羔羊至适合出口的更大体重,市面上商用轻量羔羊供给随之减少。截至7月10日当周,商用羔羊胴体溢价达到每公斤95美分。

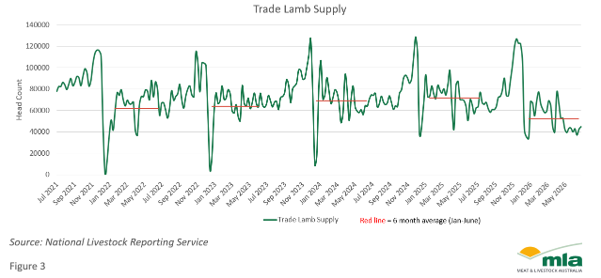

图2展示2026年1至6月商用羔羊供应量相较五年均值大幅下滑。2026年商用羔羊周均出栏量约5.5万头,远低于6.5万头的历史均值,上半年供应明显收紧。

与之相反,重型羔羊出栏量基本持平往年水平。2026年重型羔羊周均上市量5万头,五年均值为4.5万头。

重型羔羊供给远多于商用羔羊,或是两类羔羊价差持续扩大的主要原因。

全球需求与屠宰加工

价差扩大同时受到中东、北非等部分出口市场需求走弱影响。6月对上述地区羊肉出口同比下滑35%,而羔羊整体出口量同比仅下降10%。

肉类涨价叠加贸易扰动推高物流成本,部分市场价格敏感度上升,压制出口羊肉需求。与此同时屠宰加工产能缩减,加工厂收购活畜成本高企、利润承压,行业竞价热度下降。

展望后市,当前供应处于季节性低位、加工产能持续受限,且部分出口市场难以承受现有高价,羔羊价格或已接近本轮周期高点。本周商用羔羊、重型羔羊胴体单价小幅回落,分别下跌37美分/公斤、16美分/公斤。

但高端出口市场需求基本面依旧坚挺,将持续为羊肉价格提供有力支撑。未来数月,供货量与屠宰加工产能仍将主导行情走势。

信息来源:澳大利亚肉类及畜牧业协会市场信息主管 斯图尔特·布尔

数据撰写于2026年7月17日,内容截至当日准确有效

澳大利亚肉类及畜牧业协会(MLA)不对本刊物所载任何信息的准确性、完整性及时效性作出任何保证。用户使用或依赖本刊物任何内容,风险自行承担;因使用或依赖相关信息所造成的任何损失与损害,MLA概不承担任何责任。未经MLA事先书面许可,本刊物任何内容不得擅自转载、复制。凡使用MLA刊物、报告及相关信息,均须遵守MLA市场报告及信息使用条款。

消息来源:MLA

Trade lamb premium surges as supply tightens

Key points

Trade lamb extends its margin over heavy lambs by 95¢/kg cwt, the highest in more than five years.

Trade lamb yardings remain well below average, while heavy lamb supply has held firm.

Softer demand from some export markets and reduced processing capacity are limiting further price gains.

Season and supply

Favourable seasonal conditions and strong pasture growth across key southern sheep-producing regions have enabled producers to focus on weight gain while also capitalising on record lamb prices. As a result, there has been a noticeable shift towards heavier sale weights coming through saleyards compared with previous years.

The strong economic incentive to finish lambs to heavier export weights has reduced the availability of trade and lighter-weight lambs, increasing the trade lamb premium to 95¢/kg carcase weight (cwt) for the week ending 10 July.

Figure 2 highlights the decline in trade lamb supply relative to the five-year average during January to June 2026. Weekly trade lamb throughput has averaged around 55,000 head in 2026, well below the historical average of 65,000 head, indicating a notable tightening in supply during the first half of the year.

In contrast, heavy lamb throughput has remained broadly in line with historical levels. Weekly heavy lamb yardings have averaged 50,000 head in 2026, compared with the five-year average of 45,000 head.

The relatively stronger supply of heavy lambs compared with trade lambs, has likely contributed to the widening price differential between the two categories.

Global demand and processing

The widening price gap has also been influenced by softer demand from some export regions such as the Middle East and North Africa. Exports to these markets were down 35% year-on-year (YoY) in June, compared with an overall decline of 10% YoY in total lamb exports.

Increased price sensitivity in some markets, driven by higher meat prices and rising logistics costs associated with trade disruptions, has weighed on demand for export lamb. At the same time, reduced processing capacity has limited competition as processors continue to face margin pressure from elevated livestock purchase costs.

Looking ahead, lamb prices are likely approaching their cyclical peak as supply nears its seasonal low, processing capacity remains constrained, and some export markets struggle to absorb current price levels. This week, prices eased slightly for both trade and heavy lambs, declining 37¢ and 16¢/kg cwt, respectively.

However, demand fundamentals remain strong, particularly in premium export markets, which should continue to provide a firm floor for lamb prices. Supply availability and processor capacity are expected to remain the primary drivers of price movements in the months ahead.

Attribute content to: Stuart Bull, MLA Market Information Manager.

Information is correct at time of writing on 17 July 2026.

MLA makes no representations as to the accuracy, completeness or currency of any information contained in this publication. Your use of, or reliance on, any content is entirely at your own risk and MLA accepts no liability for any losses or damages incurred by you as a result of that use or reliance. No part of this publication may be reproduced without the prior written consent of MLA. All use of MLA publications, reports and information is subject to MLA’s Market Report and Information Terms of Use.

Source:MLA